“Wow, our stuff must be really heavy! This car has never had a problem getting up a hill before.”

Something felt off as we drove across town. The car was sluggish. I’d step on the gas, or try going up a hill, and it barely responded. The optimist in me thought it might be due to the weight of the tools I’d just picked up from our old apartment.

“That doesn’t smell good.”

Long story short, the front brakes had worn through their pads. As a result, the calipers rubbed metal on metal – clamping down and destroying themselves in the process. $500. That’s the bill we’re looking at to make the repairs.

The Best Camera

There’s a saying that “the best camera is the one you have with you when you want to take a picture.” That’s why we’re mostly content with whatever optics are built into our phones – they’re with us. Never mind the features available on a $200 point and shoot.

The Best Car

I think this idea applies to our car. As a family that doesn’t believe in debt, we have different options to consider when buying cars. Sure, it’d be easy to borrow money to buy a newer, nicer car. And we can afford the payments. But we don’t like the idea of indenturing ourselves. Especially not for a thing that will be worthless by the time we pay it off.

The question we faced last night was whether to put $500 into this car, or spend our savings on something else.

The Wrong Math

Our car is 13-years old. It has a leaky roof. It has a leaky head gasket (which I think should be spelled ga$ket). The driver’s door handle is broken. In excellent condition, its worth about $4,000. It’s not in excellent condition. The last time we considered trading it in, we were offered $800.

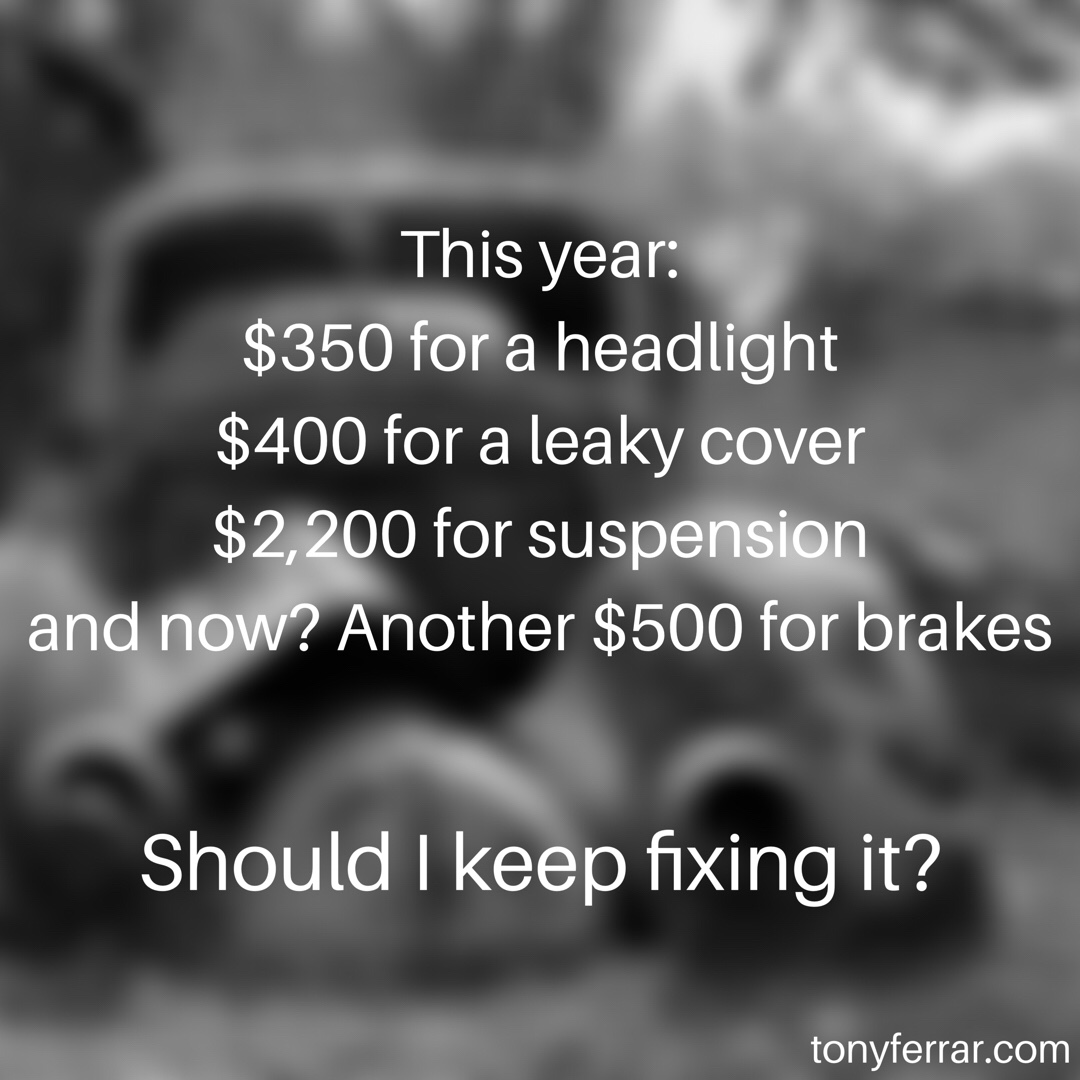

In the last year, we’ve made major repairs: $350 for a new headlight, $400 for a leaky cover, $2,200 for suspension and rear brakes. And every time we asked ourselves if it was worth it to put more money into the car.

That’s the wrong math. Cars aren’t investments. They’re depreciating assets whose value is destroyed with every mile they’re driven. You’re not going to come out on top.

The Right Math

- How much is the repair? $500.

- Do we have $500? Yes.

<li>

if not, we’d have a bigger issue to work on than our car – time to hustle up some cash with side work!

- Could we trade the car in it’s current state plus $500 for a better used car? No.

<li>

the first confirmation that fixing it is the right move

- Could we trade the car in it’s current state plus money we’re willing to spend from savings for a better used car? No.

<li>

the decision is made: fix the car

So What Does that $500 Actually Buy Us?

Patience. It gets us the chance to save a bit longer for the car we want – so that we can buy it in cash. And lest you think we’re completely nuts for investing in a car that is likely to need repairs next month, remember this: the typical car payment in America is $523/month.

If we get one more month out of this thing, we made a good deal.